The Pump Is Not the Point: What the Strait of Hormuz Crisis Is Really Costing Americans

Gas hit $4.26 a gallon and everyone is watching the pump. But the U.S. only gets 2% of its oil through Hormuz. The real crisis is fertilizer: 30% of global urea trade is trapped behind the chokepoint, there is no strategic reserve, and the planting season does not wait for a ceasefire.

The Thing You Were Told, and the Thing That Is True

When gas crossed four dollars a gallon this spring, the explanation handed to the American driver was simple: there is a war with Iran, the Strait of Hormuz is closed, and that is why filling up hurts. The first half is true. The implied causal chain is where it gets slippery, and it is worth pulling apart, because the real story is both less of a scam and more alarming than the pump-price narrative suggests.

The United States imported only about 0.5 million barrels per day from Persian Gulf sources through Hormuz in 2024, roughly 2% of total U.S. petroleum consumption. That figure is down from 0.7 million b/d in 2022, and down by more than half since 2018, as domestic shale production has surged. The blunt version: the U.S. is less exposed to a Hormuz disruption than at any point in the last 40 years. America is a net energy exporter and the world's largest LNG exporter. Almost none of the oil physically passing through that strait was ever destined for an American refinery.

So the skepticism is well-founded: the cartoon version, where a tanker that did not reach Long Beach is the reason your tank costs more, is wrong. But the conclusion that the price hike is therefore a pure scam does not quite hold either, and understanding why is the key to the whole thing. The same pattern, where official narratives are constructed to make global systemic failures feel like local supply emergencies, appears across many economic stories, as we documented in our analysis of how inflation figures are built to tell the most comfortable version of the story.

Why Your Gas Got More Expensive Anyway

Oil is priced globally. There is one world market, and a barrel's price is set by the balance of all supply against all demand, regardless of whose flag is on the tanker. When roughly a fifth of the world's seaborne oil stops moving, the global price of crude reprices upward for everyone who buys oil, including American refiners buying domestic and Canadian crude. The crude did not have to touch Hormuz. The price did.

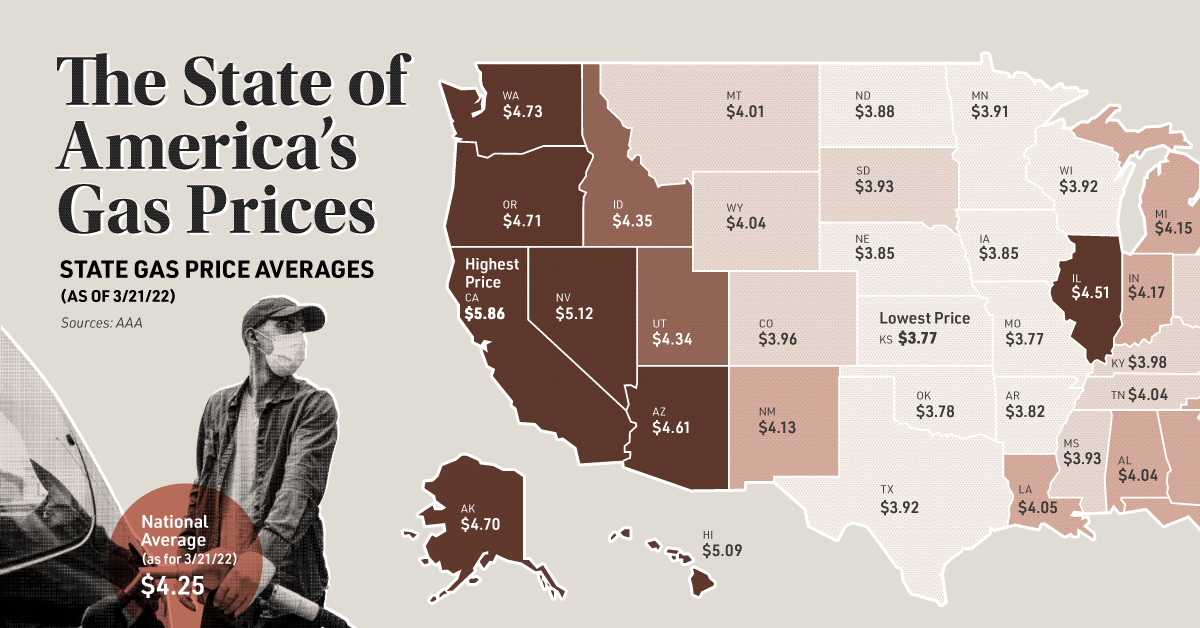

By early June, drivers in the U.S. paid an average of $4.26 per gallon for regular gasoline. The spread across the country is wide: California drivers paid the highest at $5.99 per gallon, while Indiana paid the least at $3.59. Federal forecasters have repriced the whole year. The EIA's June outlook forecasts an average wholesale gasoline price of $2.98 per gallon in 2026, an almost $1.00 increase from its February forecast, with diesel at $3.40.

On the crude side, the war moved the benchmark violently. Futures traded close to $116 a barrel, up 60% since the war began, though still below 2008's all-time high of $147.50. The forecasts for a prolonged closure are grim. The Dallas Fed estimates that a cessation of Persian Gulf oil exports lasting one quarter would raise the average WTI price to $110 per barrel, while a two-quarter outage would push WTI to a peak of $132. Wood Mackenzie's worst case is darker still: Brent crude approaching $200 a barrel by end-2026 if the Strait remains largely closed, with more than 11 million b/d of Gulf supply shut in.

The Part Almost Nobody Is Talking About: Fertilizer

Here is where the data points most sharply. The most underappreciated danger of a closed Strait of Hormuz is not at the gas station. It is in the soil.

The Persian Gulf is not just an oil hub. It is one of the planet's central factories for nitrogen fertilizer, because making fertilizer requires cheap natural gas as feedstock, and the Gulf has the cheapest gas on Earth. The concentration is staggering. More than 30% of global trade of urea moves through the Strait, along with about 20% of ammonia and 20% of phosphate. The Persian Gulf region provides an estimated 30 to 35% of the world's urea exports and about 20 to 30% of ammonia exports. One single facility illustrates the chokepoint: Qatar's massive QAFCO complex produces 14% of global urea trade single-handedly.

And crucially, there is no relief valve. Unlike oil, there are no large strategic fertilizer reserves comparable to oil stocks. Countries can release oil from strategic reserves to cushion a supply shock. There is no equivalent national stockpile of urea to crack open. Unlike the disruptions during the 2022 Russia-Ukraine crisis, fertilizer produced in the Gulf cannot easily be rerouted when the Strait is closed. Large export volumes are physically trapped behind the chokepoint. Any sustained interruption can quickly translate into higher prices and threats to crop yields and food security far from the region.

The price reaction was immediate and brutal. Nitrogen urea prices climbed above $850 per metric ton in April, up 80% since February and the highest level since April 2022. Through April, world urea prices approximately doubled and DAP prices rose about 35%.

Does This Reach the American Dinner Table?

You might expect the U.S., with its enormous domestic agriculture and gas supply, to be insulated. Partly true, partly not, and the partly not is the important half.

On ammonia, the U.S. is genuinely well-defended: it produces approximately 94% of its ammonia domestically. But urea and phosphate are the soft spots. Approximately 17% of U.S. urea consumption and roughly 20% of U.S. phosphate consumption originate from Gulf exporters whose shipments must transit the Strait. And the dependence on one supplier in particular is striking: the U.S. imports $5 billion in nitrogen fertilizers, with 51% of it coming from Qatar.

The Farm Bureau put it cleanly: fertilizer and fuel prices are largely determined in global markets, meaning U.S. farmers can experience higher input costs even when the Middle East is not the primary direct supplier. A farmer in Ohio pays the world price for urea whether or not his particular bag came from Qatar, exactly as a driver pays the world price for gasoline whether or not his particular gallon came from the Gulf. The mechanism is identical. It is just that the fertilizer version has no strategic reserve, no easy reroute, and lands on the food supply. This is the same dynamic as we documented in our investigation into how global market mechanisms produce local pain that gets misattributed to local causes.

The stakes scale up from there. Soaring fertilizer prices pressure a U.S. agricultural industry that supports 50 million jobs and over $10 trillion in output. Globally the exposure is enormous: as of 2022, Qatar's exports of synthetic nitrogen fertilizers were keeping nearly 43 million people fed in the U.S., Brazil, and India alone. One researcher comparing this to the 2022 Russia shock said plainly: "Honestly, I think it's worse."

The Two Stories, Side by Side

The gas-price story is real but self-correcting. Oil has a global price, strategic reserves exist to cushion shocks, there is an estimated 3.5 to 5.5 million barrels per day of pipeline capacity to bypass the Strait, and the U.S. sits on abundant domestic production. Painful at the pump, but structurally manageable, and it eases when the shooting stops. Prices are expected to ease in 2027 as exports recover and new supply comes online.

The fertilizer story has none of those cushions. No strategic reserve. No easy reroute, because the product is trapped behind the chokepoint rather than merely repriced. A planting-season clock that does not wait for a ceasefire. And a direct line to global food inflation, which hits the poorest countries and households hardest and lingers long after a war ends, because a missed planting season echoes into the next harvest.

The deepest irony is that the public conversation has it almost exactly backwards. The visible, dramatic, daily-updated number, the price on the gas station sign, is the part America is best protected against and the part that recovers fastest. The invisible part, the urea that quietly keeps tens of millions of people fed and that cannot be replaced or rerouted, is where a prolonged closure would do lasting damage. The pump-price narrative is busy distracting from the thing that actually cannot be fixed by releasing oil from a reserve or waiting for the next tanker to arrive.

Frequently Asked Questions

Why did gas prices spike if the U.S. barely imports oil through the Strait of Hormuz?

The U.S. imported only about 0.5 million barrels per day from Persian Gulf sources through Hormuz in 2024, roughly 2% of total U.S. petroleum consumption. However, oil is priced globally. When roughly a fifth of the world's seaborne oil stops moving, the global price reprices upward for everyone who buys oil, including American refiners buying domestic and Canadian crude. The crude does not have to touch Hormuz. The price does.

How much have gas prices risen since the Iran war began?

U.S. gasoline prices jumped by $1 per gallon in just one month following the offensive against Iran, a 34.7% increase from February's $2.98 average. By early June 2026, drivers paid an average of $4.26 per gallon nationally, with California at $5.99. The EIA's June forecast for average wholesale gasoline rose nearly $1.00 versus its February forecast. Crude oil futures traded near $116 a barrel, up 60% since the war began.

Why is the fertilizer crisis from Hormuz more serious than the gas price spike?

More than 30% of global urea trade moves through the Strait, along with about 20% of ammonia and phosphate trade. Unlike oil, there are no strategic fertilizer reserves to cushion a supply shock, and the product cannot be rerouted because it is physically trapped behind the chokepoint. Urea prices climbed above $850 per metric ton in April, up 80% since February. A missed planting season echoes into the next harvest, meaning the damage lasts long after a ceasefire.

How does the Hormuz fertilizer shortage affect American food prices?

The U.S. imports approximately 17% of its urea and 20% of its phosphate from Gulf exporters, with 51% of U.S. nitrogen fertilizer imports coming from Qatar. Prices for urea arriving via New Orleans jumped 17% soon after the war began, and benchmark nitrogen costs at U.S. ports have risen nearly 30%. Like oil, fertilizer is priced globally, so U.S. farmers pay the world price regardless of where their specific bag came from. Soaring fertilizer prices pressure a U.S. agricultural industry supporting 50 million jobs and over $10 trillion in output.

What would happen if the Strait of Hormuz stayed closed for months?

The Dallas Fed estimates a one-quarter cessation of Persian Gulf oil exports would raise WTI crude to $110 per barrel, while a two-quarter outage would push WTI to $132. Wood Mackenzie's worst case is Brent crude approaching $200 a barrel by end-2026. On fertilizer, a prolonged closure would directly threaten global food security: the Gulf's 21 million metric tons of annual urea export capacity has no alternative route and no strategic reserve backup, and the damage would outlast the conflict itself.

Kai Tutor | The Societal News Team

Follow Us!

It helps decentralize our presence across the web and it's completely free!

Instagram ➤

Youtube ➤

Substack ➤

X.com ➤

Telegram ➤

TikTok ➤