The Rise of Zombie Companies: How Fed Policy Stifles American Innovation

What Is a Zombie Company?

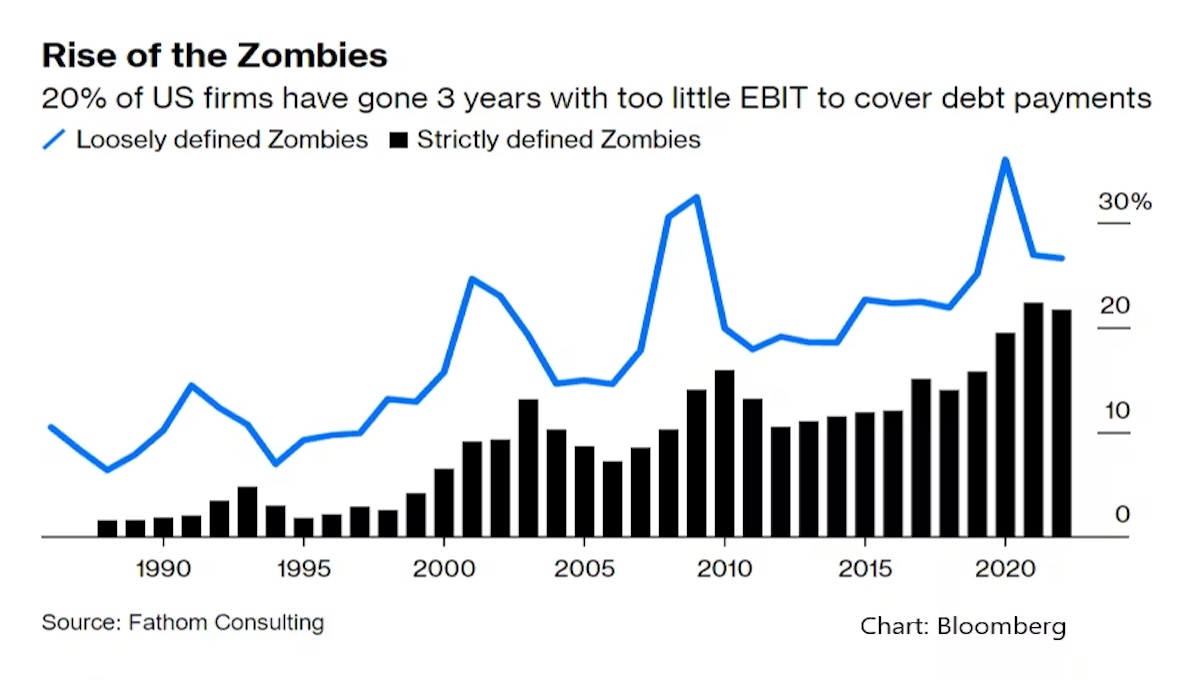

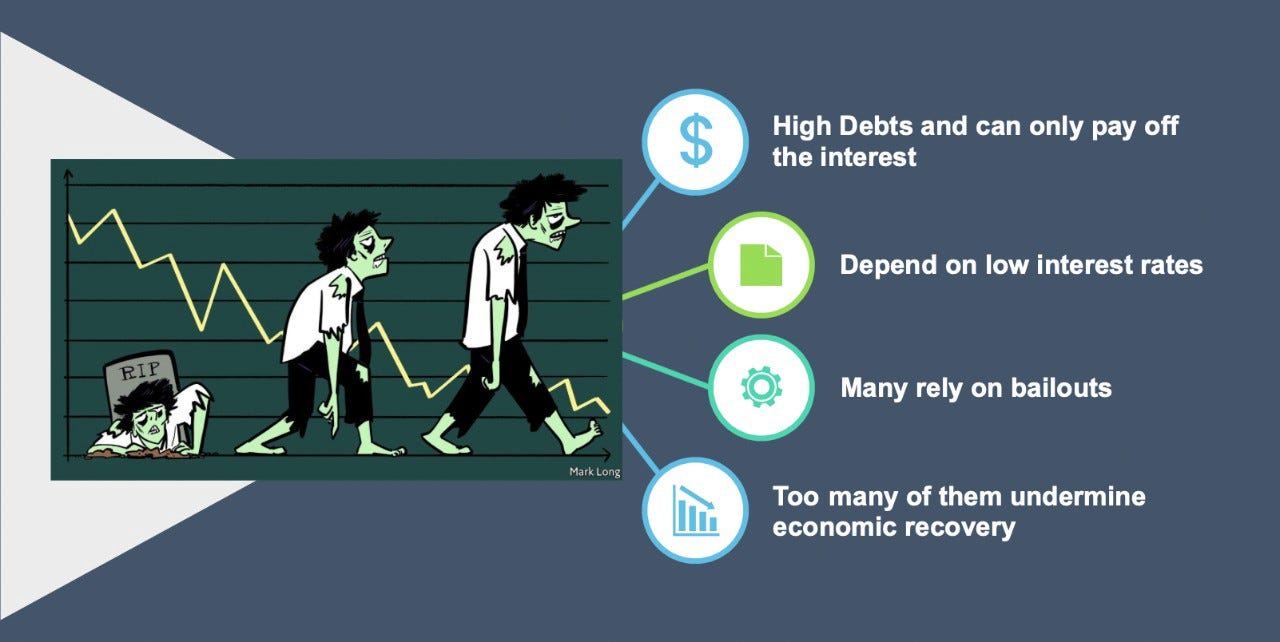

Zombie companies are mature firms — typically at least ten years old — that cannot generate enough operating profit to cover their interest payments on debt for extended periods, usually defined as three consecutive years where earnings before interest and taxes fall short of interest expenses. These companies survive not because they are viable or growing, but because they can keep rolling over debt at artificially low costs, a phenomenon first widely recognized during Japan's "lost decade" in the 1990s.

In the United States, zombies exist across public and private markets and are especially common in capital-intensive or cyclical sectors such as retail, manufacturing, energy, and biotech.

How the Federal Reserve Created the Conditions for Zombie Proliferation

The single most powerful driver of this rise has been Federal Reserve policy. Since the 2008 financial crisis, the Fed kept the federal funds rate near zero for nearly a decade, then returned it there in 2020, while simultaneously expanding its balance sheet through quantitative easing to more than $9 trillion by 2022.

QE programs — starting with $1.75 trillion in 2008–2010, followed by additional rounds totaling several trillion more — purchased vast quantities of Treasuries and mortgage-backed securities, driving long-term yields down to historic lows and suppressing borrowing costs across the economy. Corporate bond yields for even lower-rated issuers fell dramatically: BBB spreads narrowed from around 400 basis points in 2009 to 150 basis points by 2018.

This flood of cheap credit allowed struggling firms to refinance existing debt at rates of 1–3 percent — far below what their weak cash flows would justify in a normal market — and to issue new debt to cover interest payments without ever addressing underlying losses.

COVID-Era Programs Deepened the Distortion

During the COVID crisis the Fed went further, launching emergency corporate credit facilities that backstopped up to $750 billion in bonds and loans, including for firms on the edge of zombie status, and creating the Main Street Lending Program that channeled hundreds of billions to mid-sized businesses at subsidized rates.

Although these programs did not hand out literal zero-interest loans directly to non-banks, the combination of near-zero policy rates, massive liquidity injections, and implicit guarantees created an environment in which zombies could borrow at effective costs so low that bankruptcy or restructuring became optional rather than inevitable. Banks, flush with Fed-provided reserves paying almost nothing, had every incentive to roll over zombie loans rather than force defaults and recognize losses on their books.

The Scale of the Damage

The numbers are stark. US zombies employ more than 2 million workers directly, and global figures reach well over 100 million when including indirect effects in supply chains. Roughly $1.1 trillion in zombie-related debt was scheduled to mature by the end of 2025, with another large wave due in 2026.

The Hidden Assumptions Shaping the Debate

Most people misunderstand the phenomenon by treating it as a recent or firm-specific problem — blaming bad management, the pandemic, or isolated sectors — when the root cause has been sustained central-bank policy that began long before COVID. The Fed's actions were sold as necessary crisis response, but they created a long tail of misallocation that persists years later.

Hidden assumptions shape the debate. One is that low interest rates are universally beneficial rather than a selective subsidy for the already indebted. Another is the belief that central-bank interventions remain neutral and apolitical, when in reality they disproportionately favor incumbents and rentiers. A third is the short-term frame that values immediate job preservation over long-term wage and productivity growth.

Incentive problems compound the issue: bank executives prefer evergreening to protect their balance sheets and bonuses, corporate managers use cheap debt for stock buybacks that boost their own compensation, and politicians support policies that avoid visible unemployment spikes even if the cost is slower overall growth.

Second- and Third-Order Consequences

While zombies preserve jobs in the near term, they suppress real wage growth by locking labor and capital into low-productivity activities, contribute to rising inequality as returns flow to debt and equity holders rather than workers, and inflate asset bubbles that eventually burst with greater force. When defaults finally arrive, regional economies dependent on a few large zombies can suffer sharp contractions, and the public sector faces higher interest costs — already approaching $1 trillion annually in the US — that crowd out other spending.

The Risk of US Japanification

Historically, the US zombie share climbed from roughly 5 percent in the early 2000s to 10–15 percent after 2008 — a pattern that echoes Japan's experience where zombies reached 15–20 percent of listed firms and contributed to decades of sub-1-percent GDP growth.

The strongest defensible conclusion is that zombie companies represent a policy-created drag on American dynamism and long-term prosperity. Federal Reserve actions since 2008 — especially the multi-trillion-dollar QE campaigns and repeated returns to near-zero rates — have functioned as an economy-wide subsidy for unviable firms, allowing them to survive at the expense of healthier competitors and future growth. Without a decisive normalization of credit conditions and acceptance of higher failure rates, the United States risks a slow-motion version of Japan's stagnation, with productivity growth stuck below 1 percent and real GDP expansion averaging 1.5 percent or less over the coming decade.

Kai Tutor | The Societal News Team 14 FEB 2026

Follow Us!

It helps decentralize our presence across the web and it's completely free!

Instagram ➤

Youtube ➤

Substack ➤

X.com ➤

Telegram ➤

TikTok ➤