Gold, Silver & Copper | How the Metals Markets Are Being Manipulated (2026)

Organized Chaos in the Metals Markets

The metals markets are in a state of organized chaos.

The official narrative attributes all of this to geopolitics, green energy demand, and central bank buying — and those factors are real. But beneath the surface, something far more calculated is happening. The precious and base metals markets are being shaped, steered, and in some cases outright gamed by a constellation of actors: commodity trading giants, exchange operators, tariff-wielding governments, and institutional funds playing by rules that most retail investors never get to read.

Silver: The Paper-Physical Disconnect

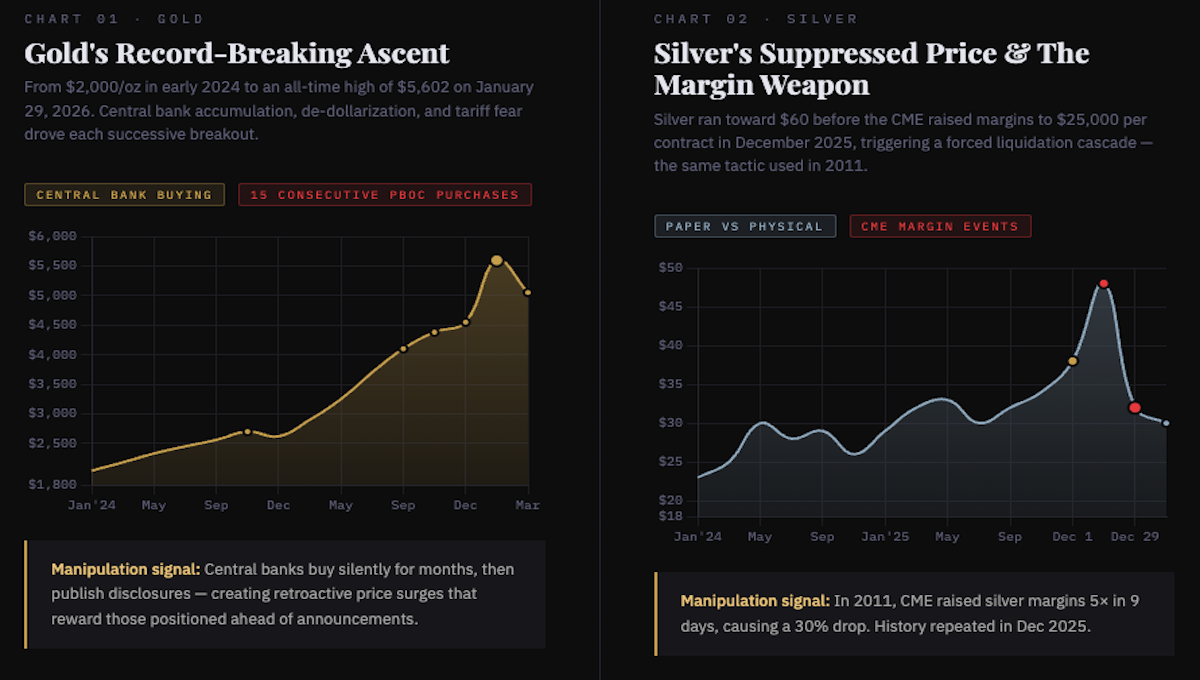

The most glaring sign of manipulation in the current metals cycle is playing out in silver. In a functioning market, price differences between exchanges should close within seconds. If silver trades cheaper in New York than in Shanghai, arbitrageurs immediately buy in New York and sell in Shanghai until the gap closes. That's market-making 101.

That is not what's happening. Shanghai has been trading at $10–$20 premiums over COMEX in New York, and the arbitrage isn't closing because when traders try to pull physical metal out of COMEX to ship east, they're discovering there isn't enough metal to move.

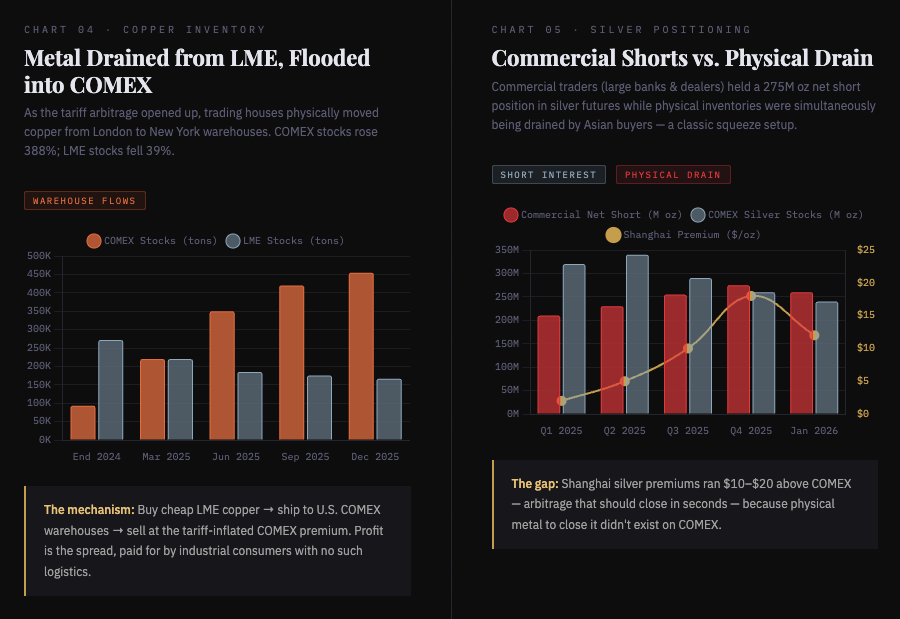

This is the hallmark of a paper market that has drifted dangerously far from physical reality. COMEX trades silver contracts, not silver bars. The vast majority of these positions are never settled with actual metal — they're rolled over, closed for cash, or used purely for speculation. The price difference between paper and physical markets is a sign of intensified demand for physical silver, particularly in Asia, where large buyers in China have been taking delivery, further draining supply available on COMEX.

The result is a market in which paper prices are suppressed relative to where the physical metal would actually trade if everyone tried to take delivery at once.

The CME Margin Hike Playbook

When prices threatened to break out, the exchange itself intervened. In December 2025, the CME Group announced it would raise the initial margin for March 2026 silver contracts to $25,000, a move that came amid rising silver prices and growing concern about market manipulation. The CME framed this as an effort to reduce speculation, but the practical effect was to increase the cost for traders betting on rising prices, forcing smaller participants with insufficient capital into liquidation.

This exact playbook was used before. During the 2011 silver price surge, the CME raised margins five times within nine days, causing a 30% drop in prices as traders were forced to sell off holdings to meet the higher requirements.

The repeated use of margin hikes as a pressure valve — applied selectively when silver rises — has fueled longstanding accusations that the CME acts to defend incumbent short-sellers rather than ensure genuine market integrity.

Adding another layer of distortion, stockpiling ahead of U.S. policy deadlines distorted both COMEX and London inventories. COMEX registered silver stock surged by nearly six thousand tonnes in a single quarter as firms raced metal into the U.S. before potential tariff duties, magnifying price dislocations between the two exchanges.

Copper: Policy-Driven Market Fracture

If silver is the case study in paper-physical manipulation, copper is the case study in policy-driven market fracture. What's happened to copper pricing since early 2025 is almost without precedent in modern commodity markets.

Copper has historically traded with tight alignment across exchanges. But the announcement of a Section 232 tariff on copper imports triggered a sharp divergence in regional prices, with the COMEX-LME arbitrage surging past 28% — an extraordinary gap for a commodity that previously averaged less than 1% spread over five years.

To understand how this happened, you need to understand the incentive structure it created. When COMEX copper in New York trades at a massive premium over London Metal Exchange copper, traders have an obvious trade: buy cheap LME copper, ship it to the U.S., and sell at COMEX prices. The pricing discrepancy caused significant challenges for U.S. recyclers and scrap processors, as overseas buyers were unwilling to pay COMEX-based prices when they could buy LME-priced material for cents per pound less.

One trading house, in a single day, drained more than a third of the world's visible copper inventory from a major exchange, then used the resulting tightness to profit on futures positions that benefited from the squeeze. Mercuria, Trafigura Group, and Glencore have systematically capitalized on these opportunities through coordinated import acceleration strategies.

This is the key mechanism. The "manipulation" here isn't necessarily illegal — it operates within the letter of exchange rules. But the effect is that a small number of commodity trading giants, with the capital and logistics infrastructure to move physical metal across oceans, can exploit policy-created price gaps in ways that distort the underlying price signal for everyone else. A manufacturer in Germany trying to hedge copper costs for 2026 is now pricing against a market that has been artificially bifurcated by tariff speculation and strategic inventory games.

Gold: Central Bank Accumulation and Silent Power

Gold's manipulation is more subtle but perhaps more consequential. Official sector activity has transitioned from sporadic purchasing to a trend of consistent accumulation, with central bank demand becoming a relevant structural factor in the global gold market, driven by a broader strategy amongst monetary institutions to diversify foreign exchange reserves.

This is not a free market at work. When the world's central banks collectively decide to buy gold and reduce dollar reserves, they are not passive price-takers — they are the single most powerful force in the gold market, and they operate without the transparency obligations that govern private traders. They don't file 13Fs. They don't disclose their positioning in real time. They can buy quietly for months, then announce their holdings, causing retroactive price surges that reward those who knew to front-run them.

Index Rebalancing: Scheduled Manipulation Hidden in Plain Sight

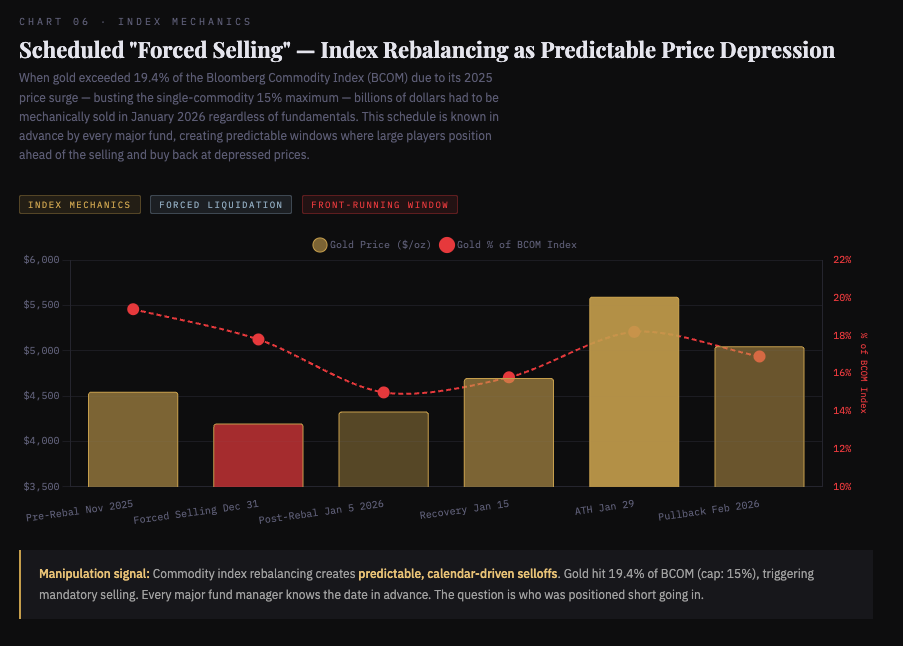

There is also the matter of commodity index rebalancing — a quarterly event that forces large, mechanical selling regardless of market conditions. Metals strategist Nicky Shiels at MKS Pamp flagged significant net selling in silver and gold futures coming in January 2026 because this year's five-decade record price gains meant that commodity-basket indices like the S&P GSCI and Bloomberg's BCOM needed rebalancing. Gold had reached 19.4% of the BCOM by value, busting the single commodity maximum of 15%.

This means that purely as a function of index mechanics, billions of dollars in gold and silver had to be sold in January 2026 regardless of what the fundamentals said. These forced, scheduled liquidations are known in advance by every major fund that tracks these indices, and they create predictable windows where large players can position ahead of the selling, then buy back at depressed prices. It is entirely legal. It is also entirely divorced from the concept of price discovery.

The White House as a Market Force

Perhaps the most underappreciated source of metals market distortion in the current cycle isn't a trading house or an exchange — it's the White House. Donald Trump's flip-flopping tariff policies on copper have decisively influenced inventory movements.

The pattern is instructive: announce a tariff, watch traders panic and flood the U.S. with metal, then suspend the tariff, causing a brief reversal, then signal it's coming back, and repeat. Each cycle of this creates enormous arbitrage profits for the few players large enough to move quickly, and enormous uncertainty costs for the industrial companies that actually need copper to make things.

For as long as that uncertainty exists, the arbitrage can continue to be broad. The ambiguity is not incidental — it is itself a market force. Sustained policy uncertainty keeps the COMEX-LME spread wide indefinitely, generating continuous profit opportunities for those with the sophistication to exploit it. Whether that outcome is intentional policy design or simply incompetent governance is a question that markets can't answer.

When silver was added to the critical-minerals list, formalizing its role in national-security supply chains, it placed silver alongside copper under Section 232 review, creating yet another layer of speculative positioning around regulatory timing.

The Narrative Machine: Banks Publishing for Their Own Books

There is a subtler form of market influence that rarely gets called manipulation but functions like it — the coordinated construction of a bullish narrative by the very institutions that profit from higher prices. This kind of commentary, published by banks with active metals desks and futures books, creates a self-reinforcing loop: analysts publish bullish calls, retail investors buy, prices rise, analysts point to the rising prices as validation of their calls, more investors buy.

Demand for copper from data centers alone was projected to reach 475,000 tons in 2026, up from 110,000 tons in 2025, according to JPMorgan — and "when developers require copper for the expansion of data centers, it is used with little concern for the copper price." The AI demand narrative is real. But it has also been aggressively amplified by institutions that hold copper futures and mining equities, and the amplification itself shapes the market.

Meanwhile, major copper mining-focused companies were pricing in a spot price of $5.49 per pound against a current price of $6.50 per pound, according to Jefferies analysts — suggesting that even the people who dig copper out of the ground didn't believe the speculative prices were sustainable.

A Hierarchy of Power, Not a Free Market

The metals markets in 2025–2026 are not simply responding to supply and demand. They are being actively shaped by a hierarchy of power: governments setting tariff policy with deliberate ambiguity, commodity trading giants using their physical logistics networks to drain exchange inventories and trigger squeezes, exchange operators raising margin requirements selectively to defend incumbent short positions, central banks accumulating silently, and Wall Street banks publishing research that supports the trades their own desks are running.

None of this is new. The metals markets have always operated this way to some degree. What is new is the scale and the speed. The COMEX-LME copper spread reaching 28%. A single firm withdrawing 35% of LME copper stocks in one day. Silver in three cities trading $20 apart with no arbitrage closure because the physical metal to close the gap doesn't exist.

As the UN's trade and development division noted, global trade may look resilient on the surface, but beneath it lies a volatile system powered more by balance sheets and financial flows than by supply chains. The physical fundamentals are real. The demand from electrification, AI infrastructure, and safe-haven accumulation is real. But the prices you see on a ticker — for gold, silver, or copper — are not a clean reflection of those fundamentals. They are the output of a system in which the largest, best-connected players set the rules, and everyone else trades in the gaps they leave behind.

This analysis draws on publicly available market data, exchange filings, analyst reports, and reporting from Bloomberg, Reuters, the Financial Times, and specialist publications through early 2026.

Kai Tutor | The Societal News Team

Follow Us!

It helps decentralize our presence across the web and it's completely free!

Instagram ➤

Youtube ➤

Substack ➤

X.com ➤

Telegram ➤

TikTok ➤